Craig DiLouie is education director for the Lighting Controls Association.

In 2021, the U.S. rebounded from 2020’s short but devastating pandemic recession with the strongest economic growth in nearly forty years. In 2022, the economy remained resilient despite high inflation and rising interest rates, ending the year on signs inflation may be easing. Due to these and other factors, global think tank The Conference Board forecasts that the economy will endure a resulting brief and mild recession in 2023 and then rebound in 2024.

A major contributor to the economy is construction, which overall exhibited very strong growth in 2022. Despite a strong finish to the year, however, nonresidential construction spending is expected to moderate in 2023 and slow significantly in 2024, according to the American Institute of Architects (AIA) Construction Consensus Forecast Panel made up of leading economic forecasters. The Panel forecasted that nonresidential construction spending will moderate to grow a healthy 5.8% in 2023 but then slow to less than 1% in 2024.

“One of the key construction storylines for 2022 was the return of enthusiasm and optimism in prospects for nonresidential growth,” said Richard Branch, chief economist for Dodge Construction Network. “While some of that will likely erode in 2023 as economic growth wanes, increased demand for some building types like data centers, labs, and healthcare buildings will provide a solid floor for the construction sector.”

2022 Construction Spending

According to the U.S. Commerce Department, U.S. put-in-place construction spending grew to a seasonally adjusted annual rate of $1.8 trillion in November 2022, the latest month for which data was available at the time this article was written. Year over year, total spending increased 8.5%.

By sector, residential construction spending grew 5.3% to a seasonally adjusted annual rate of $877 billion as of November 2022. Nonresidential construction spending, meanwhile, grew a strong 11.8% to a seasonally adjusted annual rate of $930 billion as of November 2022.

Private nonresidential construction grew 8.1% on a seasonally adjusted basis, and public nonresidential construction grew 10.4%. Overall, the top market segments were manufacturing (+42.9%), lodging (+30%), commercial (+20.3%), and highway and street (14.8%).

Click here to see the data.

Dodge Construction Network

The year ended on a positive note indicating positive momentum moving into 2023. According to Dodge Construction Network, total construction starts jumped 27% in December to a seasonally adjusted annual rate of $1.185 trillion. Nonresidential building starts increased 51%, nonbuilding starts increased 30%, and residential starts rose less than one percent.

“December starts revealed where the current strength in the construction lies: manufacturing and infrastructure,” said Richard Branch. “It is those segments that will provide insulation for the sector as the economy softens in 2023. Recession or not, higher interest rates will weigh on the economy and restrain construction starts in 2023. However, it’s encouraging to know that the new year is starting with a great deal of positive momentum.”

In December 2022, the Dodge Momentum Index (DMI) improved 6.6% to 222.2 from the revised November reading of 208.3. The DMI is a monthly measure of the initial report for nonresidential building projects in planning, shown to lead construction spending for nonresidential buildings by a full year.

On a year-over-year basis, it was 40% higher than in December 2021; the commercial component was up 51%, and institutional planning was 20% higher. In December, the commercial component of the DMI rose 8.4%, and the institutional component ticked up 2.7%.

Architecture Billings Index

Demand for design services from U.S. architecture firms continued to contract in December, according to the American Institute of Architects (AIA).

The pace of decline during December slowed from November, posting an Architecture Billings Index (ABI) score of 47.5 from 46.6 (any score below 50 indicates a decline in firm billings). The ABI was in contractionary territory for the last quarter of the year after nine months of expansionary scores.

Inquiries into new projects posted a positive score of 52.3, however new design contracts remained in negative territory with a score of 49.4.

Regional averages: Midwest (49.4); South (48.6); Northeast (46.5); West (45.5). Sector index breakdown: mixed practice (54.8); institutional (47.3); commercial/industrial (45.2); multi-family residential (44.3). The regional and sector categories are calculated as a three-month moving average, whereas the national index, design contracts and inquiries are monthly numbers.

“Despite strong revenue growth last year, architecture firms have modest expectations regarding business conditions this coming year,” said AIA Chief Economist Kermit Baker, PhD, Hon. AIA. “With ABI scores for the entire fourth quarter of 2022 in negative territory, a slowdown in construction activity is expected later this year, though the depth of the downturn remains unclear.”

Electrical industry confidence

The year 2022 posed a challenging business landscape for electrical manufacturers grappling with high demand coupled with supply chain problems, inflation, the effects of the war in Ukraine, volatile stock market, tight labor market, rising interest rates, and recession fears.

As a result, electrical industry business confidence was negative for much of the year, as expressed by the National Electrical Manufacturers Association’s (NEMA) Electroindustry Business Conditions Index (EBCI) for current conditions in North America. The EBCI was in neutral or worsening territory for 10 out of the 12 months, with December ending on a score of 50, indicating conditions had not changed from the previous month.

General Contractors

Construction contractors are less optimistic about many private-sector segments than they were a year ago, but their expectations for the public sector market have remained relatively bullish, according to the Associated General Contractors of America’s The 2023 Construction Hiring & Business Outlook.

The net reading—the percentage of respondents who expect the available dollar value of projects to expand compared to the percentage who expect it to shrink—is positive for 14 of the 17 categories of construction included in the survey.

The highest expectations among predominantly private-sector categories, with net readings of 28% each, are for power projects and other healthcare, such as clinics, testing facilities, and medical labs. There is also a generally positive outlook for hospital projects and public buildings, with net readings of 23% each. Contractors on balance were optimistic, as well, about the education sector. The net reading for both K-12 schools and higher education construction is 16%.

The net reading for manufacturing construction is 14%, compared to 27% in the 2022 survey. The net is 12% for data centers, down from 31% a year ago, and 10% for warehouses, down from 41%. There is a net positive reading of 1% for multifamily residential construction. Expectations are bearish for lodging, with a net negative reading of -4%; private office, -21%; and retail construction, -22%.

Despite the largely positive net readings, respondents are less confident about growth prospects than they were a year ago. For all but three project types, the net reading is less positive than in the 2022 survey. The steepest downturn in expectations occurred with multifamily and warehouse construction, both of which recorded declines of 31 percentage points from the net readings in the 2022 survey. The outlook for lodging construction slipped from modestly positive a year ago to negative.

“Contractors are optimistic about the construction outlook for 2023, yet they are expecting very different market conditions for the coming year than what they experienced last year,” said Stephen E. Sandherr, the association’s chief executive officer. “Even as market demand evolves, contractors will continue to be confronted by many of the challenges they faced in 2022, including the impacts of supply chain problems and labor shortages.”

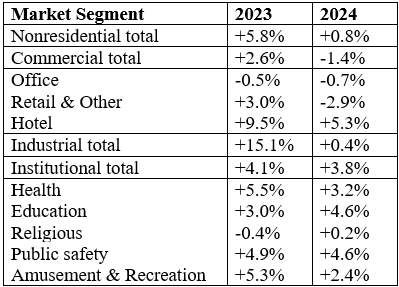

AIA Consensus Forecast for 2022

While spending on nonresidential construction picked up momentum toward the end of 2022, construction spending will moderate in 2023 and slow significantly in 2024, according to the AIA Consensus Contraction Forecast.

Despite macroeconomic headwinds such as inflation, rising interest rates, and weak consumer sentiment scores, the Forecast panel projected nonresidential construction spending to grow 5.8% in 2023 but slow to under 1% in 2024.

Similar to 2022, growth in construction spending in 2023 will be uneven with a projected 2.6% increase in the commercial sector, 15.1% for industrial facilities, and 4.1% for institutional buildings. In 2024, spending on commercial buildings is forecast to decline 1.4%, while industrial projects gain a modest 0.4%, and a 3.8% increase for institutional facilities.

“The U.S. economy will continue to face serious challenges as we move through 2023, dampening the construction outlook,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “However healthy architect and contractor project backlogs should ease the negative impact of an economic slowdown.”

Click here to see each of the panelist’s projections.