|

August 2012 |

[an error occurred while processing this directive] |

| Can Simple Payback Justify

Building Energy Improvements? It may provide some insight into a short-term project’s viability, but when used to analyze a long-term project it will most likely lead to overlooked opportunity which would have resulted in reduced utility costs and an attractive return on investment. |

David

Schurk DES, CEM, LEED AP Houston, Texas davidschurk@yahoo.com |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

When deciding whether or not to implement Energy Improvement Opportunities (EIOs), key decision makers may require that some type of economic review be performed to justify any financial investment required. With the decision to select one (or more) EIO based on this review, it is critical that all benefits be properly represented so that the project can be weighed on its true cost effectiveness.

Performing the analysis necessary to help drive an informed decision

can be both complex and time consuming. It may fall into the hands of

personnel who have had little training in performing calculations of

this type. This can result in using the quickest and simplest analysis

method that “spits out” a result, and may be one reason why the Simple

Payback Period (SPP) is so often used. The simple payback period is the

easiest method of economic analysis as shown here:

SPP= Project Cost ($) / Annual Savings ($/year)

To determine the SPP for a project you add up all the individual costs

and savings for the project each year and then divide the total cost by

the total savings. This can show how quickly an opportunity will

“pay-back” on the initial investment however it does not consider the

time value of money nor the benefits from the investment following the

payback period. This limitation means the SPP tends to favor

shorter-lived projects, a bias that is often economically unjustified.

Consider the two projects detailed below:

SPP = $5,000/$2,500 = 2 years

Each project has a simple payback period of two years, but project “B” continues to provide savings of $2,500/year for three years beyond the SPP of two years, while project “A” only provides savings for one year past the two year SPP period. The SPP method ignores critical information, such as the expected life of the project and the value to any savings after the end of the simple payback period. (1)

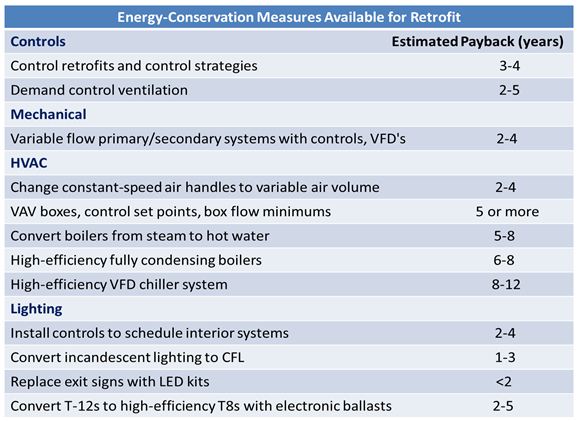

When the SPP for an energy improvement project is calculated to be between 2-3 years most companies will consider implementing it. A review of the various energy conservation measures shown in Table 1 include several which would deserve consideration based on this requirement, but by applying a strict payback criterion (e.g., all projects must have a payback of 2 years or less) are opportunities overlooked that could easily generate an attractive financial return?

Table 1: United States Building Energy Efficiency Retrofits: Market Sizing and Financial Models 2012

SPP ignores cash flows that occur past the point of capital recovery

therefore should not be used on projects with extended life

expectancies (greater than 2 years).Today’s building automation

technology evolves quickly, but it still may take from ten to twelve

years after installation before an upgrade or replacement may be

warranted.

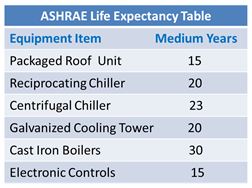

ASHRAE has published information which lists the life expectancy for

various types of HVAC equipment, ranging from between fifteen and

thirty years. This helps validate the concept that HVAC “systems” are

not short-term investments and consequently the financial benefits

derived from these EIOs can be better judged using a metric other than

SPP.

Table 2: Excerpts from ASHRAE Service Life Expectancy Table

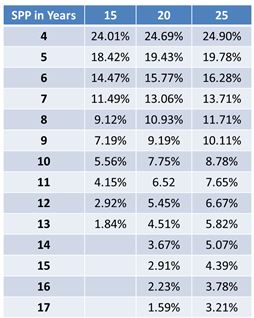

An analysis method that is used to base a project decision on the (IRR)

Internal Rate of Return* can define the interest rate or discount

rate that makes the present value of the implementation costs equal to

the present value of any project benefits. If the project earns more

than it costs to finance, it creates economic value. The internal rate

of return measures the result in percentage terms (in the form of an

interest rate)(2). The table below shows what occurs when we take a

simple payback period and calculate the projects IRR to include its

lifespan.

Table 3: Internal Rate of Return for Project Life of 15-20-25 yrs.

For example, a 7-year simple payback translates to an approximate 13%

internal rate of return (for a project with a 20-year life) if cash

flow is relatively consistent throughout the project.

The (MARR) Minimum Attractive Rate of Return (aka ”Hurdle Rate”) is the

term used which defines the “interest rate” that a company considers

acceptable, typically used to evaluate investments in new product lines

or new facilities. MARR can be company specific, often supplied by the

accounting department or from the corporate management level.

An attractive EIO could be one which provides an owner with a rate of

return equal to (or better) than that available through “other”

investment options. This makes it important to have knowledge of what

these other options are (and what they are capable of returning) in

order to compare them to any EIO’s being considered. If MARR has

been established based on exceeding net profit margins, knowledge of

the company’s profitability will help determine if the EIO will

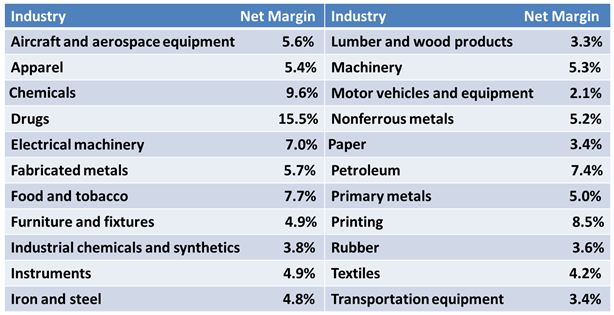

be considered attractive or not. To give a broad view of the

spectrum of profit margins for U.S. manufacturing sectors, Table 4

lists after-tax profit margins (net margins) on sales as reported for

various industries.

Table 4: U.S. Bureau of the Census, 1998.

By calculating the

IRRs that result through long-term EIO investments,

it can be noted there are many which provide returns exceeding the net

profit margin for many U.S. industry sectors (Table 4). For example, if

a textiles business has determined they will consider investments which

return 2% above their after-tax net profit margin (4.2%) they may be

willing to accept an EIO with a lifespan of 20 years and an IRR

of 6.52% (Table 3). In this case, the projects eleven year simple

payback has no real relevance in the company’s desire to return an

established MARR. Had the company instead insisted on a 2-3 year SPP

they would have overlooked an opportunity which could have met their

financial expectations.

[an error occurred while processing this directive]

Most companies have established the return they expect from their

financial investments. Armed with an understanding of these

expectations, along with the ability to analyze the economics of

various opportunities, a platform can be created from where EIOs can be

viewed by a company right alongside other investment options. Being

able to effectively communicate with key decision makers the benefits

an EIO offers when compared to a traditional investment can make the

difference between a project being shelved versus one which is slated

for implementation.

Can Simple Payback justify building energy improvement opportunities?

It may provide some insight into a short-term project’s viability, but

when used to analyze a long-term project it will most likely lead to

overlooked opportunity which would have resulted in reduced utility

costs and an attractive return on investment.

* Internal Rate of Return is only one of many analysis alternatives

used to determine the feasibility of various investment opportunities.

While not perfect, many financial decision makers use IRR when

evaluating capital projects, therefore it is a metric they may find

easy to understand. When faced with mutually exclusive projects

(projects in which multiple options exist, but only one can be chosen)

the Net Present Value method may be preferable (2). Future articles

will cover this subject in more detail.

References:

About the Author

David Schurk is a Licensed Designer of Engineering Systems, Certified

Energy Manager and LEED AP. He has more than 30-years of

energy-efficiency experience and can be reached at 920-530-7677 or

davidschurk@yahoo.com

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]