February 2011 |

[an error occurred while processing this directive] |

|

The Industry Demands Better Demand Response

In order to provide a scalable, widely-adopted and valuable Smart Grid program for the commercial building sector, the industry needs a much more fundamental increase in the intelligence of their Inside the Meter DR systems, and they need to be tightly integrated with the Outside the Meter systems as well. |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

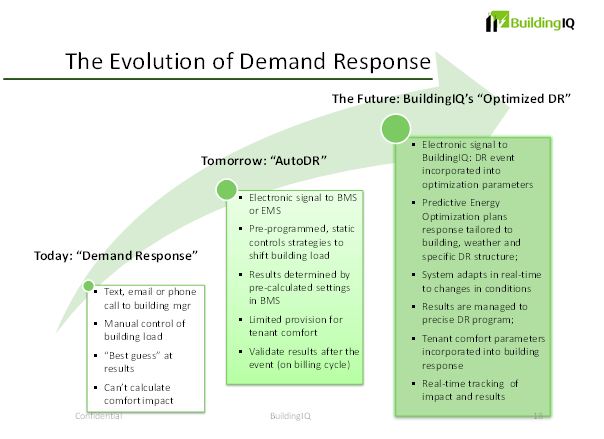

DR “successes” in our industry are trumpeted far and wide as utilities launch new programs and initial customer contracts are signed. However, there are some fundamental issues looming that have and will continue to limit the success of these programs as they are rolled out across the commercial building sector. There are enormous challenges, namely:

Despite the potentially huge scale of DR programs and dollars in our

industry, the current technologies and systems in place to help

utilities and the commercial building sector execute DR programs are

surprisingly rudimentary. Examples of this “Manual DR” are:

How can building owners confidently participate in DR events this way?

How can a utility build a scalable, effective DR program reaching the

hundreds or thousands of customers they need to on these sorts of

mechanisms? They can’t. Talk to commercial building owners or

utilities, and you will learn that the commercial sector has not been

adopting DR programs nearly as much as one would expect. For example, I

recently spoke with one of the top 5 direct property investors in the

world, and they noted that they had only one building in the U.S. on a

DR program, since that was the only one that had a building manager who

knew the building and its systems well enough to manage through an

event (they have since stopped participating).

This lack of adoption is one of the big reasons for the introduction by many leading utilities of the Peak Day Price (PDP) tariff program which charges 10-15x the normal rates during peak periods. Unlike the voluntary incentive programs, large commercial customers are automatically moved onto the PDP program unless they opt-out by adopting another DR plan.

Why are the DR programs not working? Basically because current energy

management systems and practices in the commercial sectors were not

created for a world with DR (or for interaction with any external

system, for that matter). The vast majority of the recent innovation

from the industry has been coming directed “Outside the Meter” (outside

of the building) from leaders such as EnerNOC or Comverge. But in

reality, these DR programs will not succeed unless there is a

corresponding amount of innovation “Inside the Meter.” Inside the Meter

is the domain of vendors like Honeywell, Schneider-Electric and Johnson

Controls who, though large companies with broad offerings have

difficulty moving very quickly to innovate, and don’t have a lot of

incentives to radically change their mature, stable and fairly

concentrated industry.

To their credit, a number of these companies are now starting to focus on these problems either individually, through partnerships or acquisitions. Thanks to the work of government labs like Lawrence Berkeley, industry bodies and some leading vendors, more intelligent automated solutions and standards like OpenADR are being piloted in the market, but things are moving slowly. Even these emerging “AutoDR” solutions still leave much to be desired, as they basically consist of:

But have:

[an error occurred while processing this directive] In order to provide a scalable, widely-adopted and valuable Smart Grid program for the commercial building sector, the industry needs a much more fundamental increase in the intelligence of their Inside the Meter DR systems, and they need to be tightly integrated with the Outside the Meter systems as well.

This next generation of DR might well be called “Optimized DRTM”. Components will need to include:

If the industry is to deal with these major barriers to adoption and

achieve its potential in terms of the Smart Grid, it must move from

“Manual DR” and the emerging “AutoDR” to the future’s “Optimized DRTM" for commercial buildings. While my company, BuildingIQ, now

offers “DRIQ,” the world’s first Optimized DRTM solution (see

www.BuildingIQ.com), we need a range of solutions from the major Inside

the Meter vendors to move the industry forward.

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]