November 2006

![]()

AutomatedBuildings.com

[an error occurred while processing this directive]

(Click Message to Learn More)

November 2006 |

[an error occurred while processing this directive] |

|

|

Paul Mason |

BuilConn Europe 3-5th October 2006

CONNECTIVITY WEEK included an IBX forum where the final session was

“The Roadblocks and How to Overcome”

The concept of intelligent buildings, (maybe now we can term them “i.p.-buildings”? or 3G intelligent buildings), has been around for many years.

However the application of intelligence in buildings has yet to deliver its true potential. It is still the case that the Funders of projects and the Developers of projects still do not see the benefit of i.p.-buildings, they have hardly heard of them!

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[an error occurred while processing this directive] |

This roadblock session of the IBX forum, CONNECTIVITY WEEK, looked at some effective implementations of intelligent building solutions and the session discussed the strategy to overcome the roadblocks. The session looked at some technologies required to deliver truly integrated ICT / BAS intelligent building solutions.

A general case study on roadblocks was the brief given to Paul D.J. Mason who presented some projects in technical terms and then reviewed the benefit/value propositions for each of the main stakeholders of those projects.

Paul D.J. Mason first attempt at an I.P.-building was BA Waterside, this building was opened in 1998. The building automation and ICT design of this project was first considered in 1993, DEC and their solution was considered along with the market at that time. The I.P. building automation solution that was considered was with the Company CDC and using PC motherboards in the risers. This i.p.-building attempt failed on the principle that the employer’s top motivation was no lock-in to any particular service provider, general inter-changeability / inter-operability was the goal, as well as cost benefit of course.

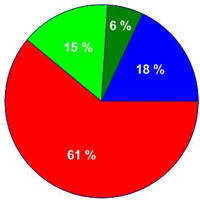

Since and including BA Waterside there have been 10 years of finished buildings by Paul D.J. Mason and his staff, the value in fees has been in the order $22.8m and with a project value in the order of $1.52b total which was used to build out some 456,000m2 area overall. The proportion of building automation systems executed by Paul and staff over the last 10 years can be divided into proprietary systems and open systems and this splits as 61% proprietary to 39% open systems.

The analysis by building area (179,000m2 open systems

over the 456,000m2 total) installed last 10 years by Paul and Staff reveals 4

beneficiaries:

The analysis by building area (179,000m2 open systems

over the 456,000m2 total) installed last 10 years by Paul and Staff reveals 4

beneficiaries:

|

1. |

contractor cost benefit |

15% |

|

2. |

employer cost benefit |

6% |

|

3. |

funder/developer benefit |

0% |

|

4. |

end-user no-lock-in / flexibility benefit |

18% |

|

5. |

no intelligent building benefits (simple conventional) proprietary systems |

61%. |

The data, top ten buildings listed by way of example of the buildings in the sample:

|

BA Waterside |

1998 |

50,000m2 |

opened by the Prince of Wales July 1998, End user, British Airways HQ |

|

Ibex House |

1999 |

20,000m2 |

Refurbish in-situ floor by floor, various |

|

18 Bevis Marks |

2000 |

3,500m2 |

End user, Re-insurance Co. HQ |

|

48 Warwick St |

2001 |

3,500m2 |

Speculative Development, The Crown Estate |

|

Lunar House |

2002 |

40,000m2 |

End user, Immigration Dept. HQ |

|

21 Tudor St |

2003 |

9,000m2 |

Pre-let, Int’l Lawyers Jones Day UK HQ |

|

Clive House |

2004 |

10,000m2 |

End user, Justice Department HQ |

|

2 Marsham Street |

2005 |

75,000m2 |

Proprietary Systems, Interior Department HQ |

|

16 N.Burlington Pl. |

2006 |

4,000m2 |

opened by the Prince of Wales June 2006, End user, The Crown Estate HQ |

|

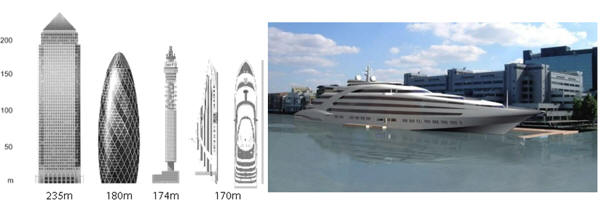

SuperYachts |

2008 |

20,000m2 |

Many designs and global locations, First: West India Dock, London |

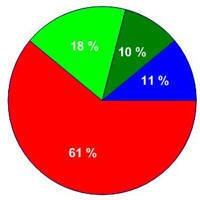

Proprietary

Systems 61% by building area

Proprietary

Systems 61% by building area

Open Systems Building Automation

by building area and split into

Public and Private Sectors and hew or refurbishment

Private New Build 18%

Private Refurbishment 10%

Public New Build 0%

Public Refurbishment 11%

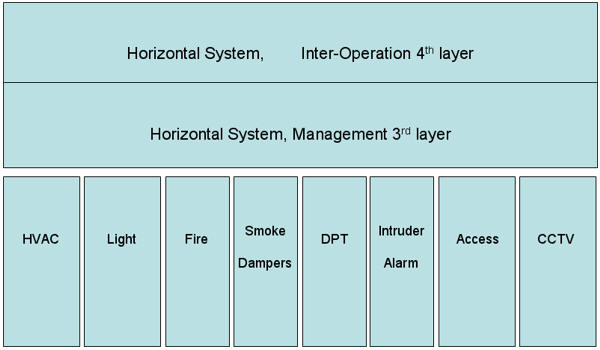

The type of systems installed, showing the development from no co-existence to BAS convergence and IP backbones and incorporation of fire alarm systems

|

BA Waterside |

1998 |

BMS, Lighting |

and Access Control all LonWorks and 1.2Mbs LON backbones in parallel, no in-op or co-ex |

|

Ibex House |

1999 |

BMS only |

multi-product, shell and core with LON backbone arranged for floor by floor refurbishment |

|

18 Bevis Marks |

2000 |

BMS, Lighting |

and Access Control all LonWorks and inter-operation with BMS and Lighting, Co-ex with Access Cntrl |

|

48 Warwick St |

2001 |

BMS, Lighting |

and Access integrated also with DPT, Lift controls, WEB service |

|

Lunar House |

2002 |

BMS, Lighting |

fibre optic backbone arranged for in-op but lighting opted to run standalone |

|

21 Tudor St |

2003 |

BMS, Lighting |

shell and core. Tenant opted for Trend in their fit out on BMS connecting into hubs, 3 per floor & 5 floors |

|

Clive House |

2004 |

BMS, Lighting |

with Fire / PIR / Temp interoperating (Zytron) |

|

2 Marsham Street |

2005 |

Proprietary BAS |

BUT very modern ICT, highly converged ICT |

|

16 N.Burlington Pl. |

2006 |

BMS, Lighting |

and Access with Fire / PIR / Temp integrated also with metering, stair vent, DPT, Bomb alert, Lift controls, WEB |

|

SuperYachts |

2008 |

BMS, Lighting |

IP to controllers, one per room, cross connects to Fire on LON, LonMark System inter-operability |

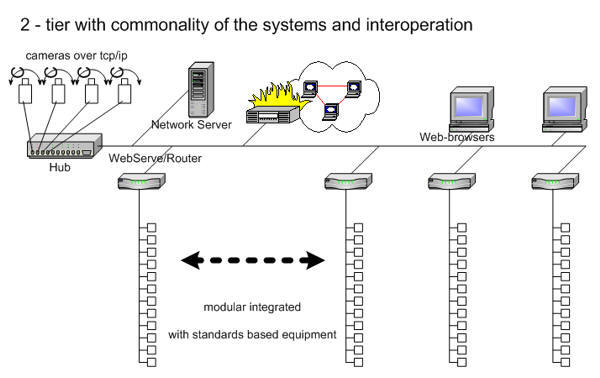

The system strategy installed all open systems:

|

web services and the network boxes, I.P., Ethernet |

|

cable infra-structure, standards compliant throughout |

|

standardised products c/w with s/w ready for

customisation |

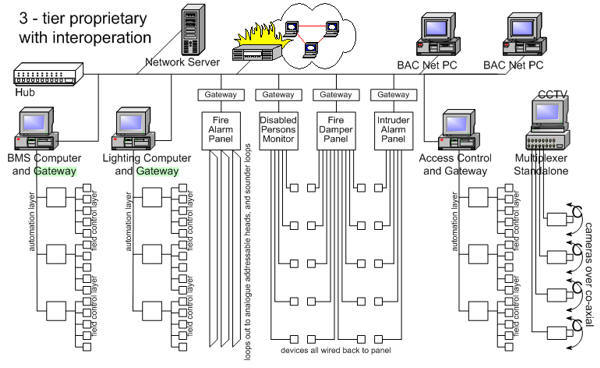

The proprietary system installation strategy, any management network or inter-operation was installed post-contract.

List of benefits, arranged appropriate to the class of beneficiaries:

|

Owner / End, |

user Freedom of choice, no extra cost, better value, future proof |

|

Investor, |

None established or proven |

|

Developer, |

None established or proven |

|

Cost Consultant, |

Capital Cost is same or lower, running cost is lower |

|

Manufacturer, |

Standards best for manufacturer, OEM commodity market |

|

Manufacturer & Contractor, |

None established or proven |

|

Designer, |

Simple modular, scalable, standards based, best for Clients |

|

Contractor, |

None established or proven |

|

Facilities Manager, |

Freedom of choice, running cost is lower, future proof |

|

Government, |

Building Regulations require working controls / documented |

[an error occurred while processing this directive] List of roadblocks with respect to the class of beneficiaries:

|

Owner / End, |

Investors /Developers /Cost Consultant /Manu.&Contract. / Designer /Contractor will not “champion” ip-buildings for Owners |

|

Investor, |

Never “heard” of ip-buildings |

|

Developer, |

Never “heard” of ip-buildings except do they cost more? |

|

Cost Consultant, |

Not their responsibility, understand but not their risk to take |

|

Manufacturer, |

Will prefer to provide solutions that require higher lock-in cost |

|

Manufacturer & Contractor, |

No preferential lock in to up to 10% p.a. service deal and no knowledge about maintaining other companies products |

|

Designer, |

Will not learn, do not want to learn, not their problem ? (Yet) Except for a few Designers who get it ( but need interoperability) |

|

Contractor, |

Most do not care/understand / not their problem, they prefer low technology, Except for a very very few Contractors who get it |

|

Facilities Manager, |

Not powerful at the CapEx stage, too expensive to fix at OpEx |

|

Government, |

Education in all matters science / technology / construction |

|

The solution:

disruptive change is necessary over the whole globe/planet, i.e. all BAS/ICT systems to be supplied by large ICT systems integrators, bought by the main contractor (new build) or FM departments (in-situ refurbishment), procurement change is necessary, buy all ELV from one source, cables / duct / pipes from others (buying higher technology services from low tech people is expensive and very risky (they can not make it work / do not understand).

disruptive change is necessary, go to all IP backbones, 4th utility strategy, all package plant to be inter-operable, inter-operability is the key requirement, always was always will be – on common media and transport systems e.g. Cat 6, Ethernet, TCP/IP, suggest oBiX2 at the higher end of inter-operability.

funding agencies, developers and property agents all need to be convinced of that there is class A*star building and that these are i.p.- buildings and that the current crop of so-called class A developments are in fact less valuable to the End-users. i.p.- buildings have the 4th utility plumbed in and are converged as a matter of normality and that by design they cost no more than last year’s “Class A” building but provide great adaptability to End-users.

The SuperYacht project, http://www.aquiva.co.uk is one such i.p.- building project, a 3rd Generation intelligent building. The first is located in West India Dock, London, this is a 5-star LUX hotel making great use of the quayside site available.

I.P. down to room automation controller, to TV and AV, to high-speed internet, to phones and WiFi Access points, to guest digital assistants, to RFID and EPOS, and to each plant room as arranged as an I.P. node. Inter-operability uses the LonMark System profiles, Lighting sub-net work is DMX for the all LED low energy system.

Built on a global manufacturing strategy for best cost and quality materials and performance.

[an error occurred while processing this directive]

About the Author

Paul D.J. Mason

“Designer”

Paul D.J. Mason, B.Eng (Hons), is a consultant for i.p.-buildings and a MEP designer, currently the designs being pursued by Paul are all innovative solutions in the marine engineering environment with floating structures, pier structures and shore-side infrastructure projects around the world.

Mr. Mason’s career encompasses Marine Engineering Royal Navy 1975-81; the Property Services Agency of the UK Department of Environment 1982-86; University as a mature student 1986-89; then MEP design and associate director at CJP 1989-97, MEP design and CEO at BWP plc 1997-2005, then 2005-06 CTO at I2S assisting the merger ESL/ITM/Massa Solutions into I2S.

Mr. Mason is now working directly with the Owners and Partners of Aquiva Developments Ltd. Mr. Mason has been a contributing editor of AutomatedBuildings.com, he authored the LonMark virtual building headquarters cost comparison model and is honorary life vice-president of LonMark UK.

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]