With all the post-COVID increases in vacancy rates in major metropolitan areas, a new, more comprehensive yardstick for valuation of a commercial building is necessary. These vacancy rates which we are seeing in many metropolitan areas are not going to go away anytime soon and the impact to the building’s worth is significant. No appraisal system has been developed to take into consideration this new permanent variable. Those who “claim to be experts” should open up their eyes and realize when a paradigm shift happens, old rules-of-thumb and yardsticks to measure value, become obsolete. You might as well put a horse-and-buggy picture on them because that’s how relevant they are in this new post-Pandemic commercial real estate marketplace.

Unlike some long-time veterans of the commercial real estate market, I do not believe we are going back to “Business-as-usual”. Too many companies in various sectors have opted to go with having a good percentage of their workforce work-from-home permanently. They have seen both gains in productivity as well as real expense costs cut down from reducing their corporate footprint in commercial leasing.

Much of the commentary here is based on reading the comprehensive guide to commercial real estate evaluation techniques in the article, Commercial Real Estate Appraisal: A 10 Point Guide to CRE Valuation (https://www.startdeck.com/blog/commercial-real-estate-appraisal-a-ten-point-guide-to-cre-valuation/#Establishing-the-Commercial-Appraisal-Scope-of-Work ) as well as the CCIM’s article on Valuating Vacancy (https://www.ccim.com/cire-magazine/articles/valuing-vacancy/ )

Both articles go into a well-detailed approach on how to come up with a value of a building in a traditional sense with various determinants being part of the overall evaluation. What they don’t discuss is the profitability of the building becoming a more important factor when it starts to lose occupancy and that vacancy becomes more permanent. The increase in vacancy rates should become a determining factor, especially if they represent a new trend within the area which is not going to go away within a quarter or two. This is the reality we are facing today, and most 30-year “experts” are not including this in their formula.

The big question to appraisers become, “What is the “additional discount” applied for Vacancy Rate?” How does a fully leased-up building differ than one that is only 70% occupied? What is the additional discount rate if that occupancy rate slides to 60%? 50%? 25%?

In earlier articles I have observed, when it comes to leasing up commercial office space in buildings, more space is becoming available to a lesser-and-lesser demand: “the Reverse of Musical Chairs” .

We have more and more companies utilizing people in work-from-home positions, and they are reducing their need for office space. For example, American Family Insurance has a 40-building campus around Madison, Wisconsin. They now only occupy six buildings out of the forty that are there. Who is going to occupy the other 34 buildings?

There would have to be a huge demand for office space from several large companies like Facebook, Google, Amazon, and others in order to fill up those buildings. That is not happening and that is only one campus which has lost occupancy. How many downtown buildings and suburban office campuses are facing the same levels of vacancies across the country?

In many cases, organizations are shrinking their corporate footprint substantially. Since 2021, some companies have minimized their corporate footprint in commercial space by 50% or more. As others do this, office space becomes more and more available to a lessening market demand. Plus, that demand is for buildings which can support corporate mission critical applications.

Mission critical applications require redundant power and connectivity coming into the building. If a building does not have that, it is considered technologically obsolete and more likely to remain permanently vacant because no company can afford a single point-of-failure within a building that will impact their mission critical applications.

From the article, What is Breakeven Occupancy in Commercial Real Estate?

(https://fnrpusa.com/blog/break-even-occupancy-commercial-real-estate/ )

For an income producing property, breakeven occupancy is the point at which a property goes from an operating deficit to an operating profit. Mathematically, it is calculated as total operating expenses plus debt service, divided by potential rental income.

This sort of analysis is used by lenders and investors as part of their underwriting process to establish the occupancy boundaries for a property.

As a general rule-of-thumb, the lower the breakeven occupancy ratio, the better. In the normal course of business, most break-even ratios fall in the range of 60% – 80%.

HOW TO CALCULATE BREAKEVEN OCCUPANCY

To measure breakeven occupancy, many investors use the “breakeven occupancy ratio,” which is calculated as: Breakeven Occupancy Ratio = (Total Operating Expenses + Total Debt Service) / Potential Lease Income

Example — total expenses plus debt service divided by potential rental income equals the breakeven occupancy ratio. For example, suppose a property had

$400,000 in operating expenses,

$250,000 in debt service, and

$1,000,000 in potential rental income. The breakeven occupancy for this property would be:

Breakeven Occupancy = $400,000 + $250,000 / $1,000,000

The result is 65%. This means that any occupancy level above 65% would signify that the property is producing a profit. Anything below means that it is producing a recurring loss.

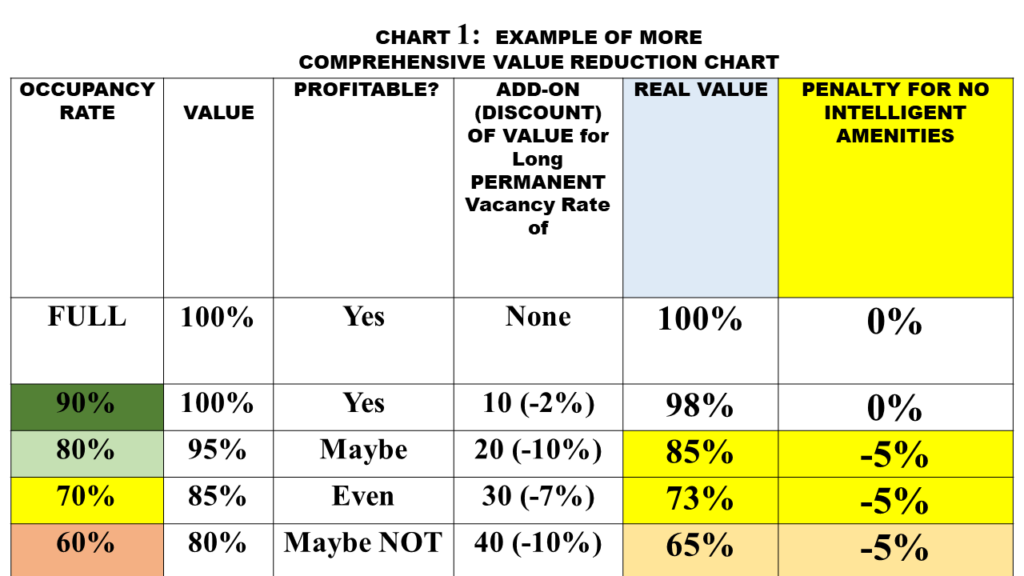

What if we ADD other variables that would affect that property’s profitability goal? What if we added a percentage of loss, if there was a significant permanent amount of vacant space?

Should it be 20% if there is 20% Vacancy (a one-to-one ratio)

OR – if it is MORE significant than a 20% Vacancy rate, should the discount then go to a graduated ratio? l.5 to l from 25% vacancy? (i.e. 26% vacancy = 39% discount in value. 40% vacancy drops the discount in value 60%) In addition. should there be an extra penalty of reducing the value of the building if it lacks “INTELLIGENT AMENITIES” like redundant power and high-speed broadband connectivity coming into it? (See CHART I)

Source: James Carlini

Another variable that needs to be adjusted is the debt service portion of the formula. When you have the “cost of money” go from 3% to 7% or more, that is going to weigh heavily on determining the breakeven occupancy number.

Taking the same example from above, but doubling the Debt Service number, we see a significant change in the result of what the “Breakeven Occupancy” number should be:

$400,000 in operating expenses,

$500,000 in debt service, and

$1,000,000 in potential rental income. The breakeven occupancy for this property would be:

Breakeven Occupancy = $400,000 + $500,000 / $1,000,000

The result is 90%.

So if you have a highly vacant building, let’s say 30% occupied with the original formula was looking at 65% as the building’s Breakeven number pre-COVID, and now you have lost tenants from an original occupancy of 75% (which was profitable) to 30%, not only are you losing money monthly, if you go to refinance and the rate is double or more than what you have in the original formula, you need to add more new tenants (increase occupancy from 30% to 90% just to break even). Accomplishing this in a shrinking market is just about impossible.

It’s impossible to do in the current market because there is also a shrinking amount of demand and you will NOT be able to sustain the lease rates that you had prior to COVID because there are twenty similar buildings to compete with for the same tenant. This is the result of the concept of the “Reverse of Musical Chairs” when it comes to demand. You have more and more space coming available on the market, with less and less demand because many companies have cut their requirements for office space. Price per square foot will go down substantially.

The remaining corporate tenants looking for space in the market will expect a lot cheaper lease rates, especially if your building cannot provide the intelligent amenities of redundant power and broadband connectivity. AND that further destroys any chance of getting back to profitability. You cannot have an Occupancy Rate of 130% to attain a “break even level”.

This is why some owners are dropping off the keys to big buildings to the banks. They don’t see profitability on the horizon. The big question becomes. “How much of a discount are you going to apply to the price tag of the building?”