|

September 2012

Article

AutomatedBuildings.com

|

[an error occurred while processing this directive]

(Click

Message to Learn More)

|

ESCO 2.0 and Your Next Project

In terms of a business model focusing on implementation of efficiency,

renewable energy resources, and financing vehicles for capital upgrade

projects, the Energy Service Company (ESCo) model is seeing a

resurgence among building owners.

|

As

published

June

Issue

|

Previously in

Engineered Systems, Leighton Wolffe presented ideas and

perspectives on high performance buildings and the convergence of the

IT, Energy and Building Technology industries in the new smart grid

environment. In this article, Leighton and Jack McGowan team up to

provide insight on how facility owners can make sense of the many

energy related services and programs to help finance capital

improvement projects and infrastructure upgrades to achieve high

performance buildings and campuses.

For

facility professionals every mechanism to make capital improvement

projects a reality is worthy of attention. However, this has become a

rather complicated formula to master; with the array of vendors, energy

suppliers, service providers, demand response companies, dashboards and

analytics programs, and building automation manufacturers all claiming

to be the key component when it comes to providing comprehensive

benefits and improvements to operations and energy.

While each element of the energy equation is important, questions immediately start to arise such as:

- ECM’s – how to prioritize?

- What if I choose a dead-end technology?

- How does this all get integrated together?

- How do I differentiate between Vendor A and Vendor B?

- How can I avoid getting locked in to something that does not

perform?

These are just a

few of the considerations important to the stakeholders responsible for

finance, operations, energy procurement, labor negotiations, risk and

life safety, contract management, and other departments in facilities

that influence and drive the decisioning process.

As every facility

manager knows, without an adequate operating budget, it isn’t possible

to maintain buildings and equipment. Hand in hand with the operating

budget is capital, which is harder to assemble in this economic

climate, but must be available to renew and upgrade infrastructure. In

this complex environment, building owners are constrained, but open to

proven business models that can have positive impacts on both

budgets. Using traditional channels, the justification and

approval process to get funding is a time consuming and multi-hoop

endeavor even in the best of times. Elevating a typical building to

“high performance” is an even more complex undertaking that requires

sophisticated interoperability between dissimilar equipment and

systems.

A basic dilemma

faced by owners is choosing between maintaining a legacy system or

moving to high-performance technologies to replace equipment. The

economics that support this decision process are not as clear or well

defined as the simple ROI we are all used to – Efficiencies and avoided

costs after project installation equals savings that pay for the

project.

When the concept

of implementing smartgrid technology is introduced, the issues around

justifying expenditures increase. When renewable energy and distributed

generation resources become part of the project scope, the complexities

around financial modeling become exponential.

It seems that most

vendors can only offer slices of the project, and that price and cost

of aligning multiple vendors together can quickly outweigh the benefits.

Accordingly, a

number of companies that serve this space are looking at providing more

end to end solutions and are starting to offer software and hardware

applications that serve the entire energy chain from supply side power

purchasing to demand side load control, energy efficiency measures and

capital asset management. With all of these options, the

questions become “ Who is the prime vendor, what technologies do we

use, how does this all fit together, and how are we going to pay for it?

In terms of a

business model focusing on implementation of efficiency, renewable

energy resources, and financing vehicles for capital upgrade projects,

the Energy Service Company (ESCo) model is seeing a resurgence among

building owners. This is particularly true for owners that have

scarce capital and marginal credit ratings. That said, Energy

Services is a broad topic and includes a wide range of offerings, but

at its heart the model entails a combination of three critical

elements. Those elements are: 1) engineering self-funding energy

measures, 2) financing based upon a revenue stream (typically from

savings that are calculated and, in some cases, guaranteed and 3)

implementation. During this time of continuing stress on capital

project funding, Energy Services is seeing an evolution in its

financing optionalities, beyond the “plain vanilla” versions,

increasingly towards what is becoming known as ESCO 2.0.

ESCO 2.0 is a

variation on the proven theme that has been called Performance

Contracting over the past three decades. The “2.0” is an

outgrowth of Web 2.0, which according to Wikipedia “is a loosely

defined intersection of web application features that facilitate

participatory information sharing, interoperability, user-centered

design,[1] and collaboration on the World Wide scale.”

With ESCO 2.0, access to the Web is critical, but the “application

features” in this case are designed to access new revenue streams and

create larger more exciting capital projects. So the ESCO 2.0

phenomenon seems to be upon us, and forward looking companies have

embraced it by incorporating Smart Grid and Demand response strategies

to tap into positive cash flow revenue stream that is creating a 2.0

self-funding matrix. Of course Energy Service Companies or

“ESCO’s” are those organizations that specialize in delivering this

model, but of course all ESCO’s are not created equal.

This article is

intended to reacquaint the reader with the complex topic of Energy

Services, and to cover some of the evolution that has occurred in

recent years. If the reader has not kept abreast of those

changes, it is time to do so, because it could make the difference

between go and no-go on your next project. We will revisit the history

of Energy Services or Performance Contracting, address current ESCO

Best Practices and describe the Next Gen ESCO 2.0 models that are a

best kept secret.

History

[an error occurred while processing this directive]Energy

Services may be one of the most exciting concepts to hit the energy and

buildings business over the last several decades. Yet this

business model, and the industry that it spawned, has experienced many

transitions over that time and recent studies of Performance

Contracting, combined with general observations of trends, indicate

that many projects are doomed to languish without it. Equally

important, energy services is poised for a next wave that will be

characterized by broader forms of both technology applied and financing

approaches used. Integral to these new elements with be

traditional efficiency coupled with Demand Response using the OpenADR

Standards to leverage more Smart Grid Functionality, which will

contributed more dollars to the financing pool. Before exploring

all of these developments however, it may be helpful to revisit the

origins of this model. Energy Services seems a timely topic, but

the model itself has been around for decades. This method

of implementing energy, and Capital, projects originated in Europe

after World War II, when it was called “chauffage.” Chauffage

means “heat” in French, but at that time the idea was to address two

major challenges: the need to rebuild and renew capital infrastructure

that was ravaged during the war years, and the need to control

astronomical energy costs for building owners. Chauffage was a solution

that provided building owners with energy sources, delivered by a third

party that turn keyed the engineering, facility management and

financing for projects. At the same time, the model provided

entrepreneurs with the opportunity to convert the risk associated with

building renewal into a viable business opportunity. The term

win-win could be used because building owners got problems fixed,

investors made money and the workforce got jobs

The concept of

Energy Services or Performance Contracting came to the U.S. in the late

1970’s under a different name “shared savings”. Shared savings is

a concept that has seen some resurgence recently, in the form of Power

Purchase Agreements (PPAs) for renewable energy. Uncertainty in

the energy markets, impacted by dramatic changes in oil / gas supply

and energy price drops in the mid-1980’s, resulted in changes to the

model. As a result of unpredictable price volatility, the

industry decided that it would exit the business of speculating on

energy futures and focus on engineering of self-funding

projects. As a result the Energy Services mode developed,

sometimes referred to as performance contracting. This is usually

where a story reads, “And the rest is history.” However, that’s not the

case for performance contracting because new electricity programs from

Rebates to Demand Response are positioning the industry to enter a new

frontier.

A key point with

performance contracting is that the ultimate technology limiters have

to do with energy cost and the enabling legislation in a particular

state. (Readers who want to learn more about enabling legislation in

specific states may start by visiting; http://www.dsireusa.org

and clicking on the states of interest.) Critical aspects of the

legislation, such as the term (number of years) that is enabled for

such agreements and the types of energy measures that are allowed, will

define the technologies that can be implemented. By the same

token, the local cost of energy (particularly electricity), and the

presence of utility rebates are also factors.

In addition to the

site above there are a number of other sites containing a wealth of

information available over the Internet. Two Web sites that include

great data on performance contracting are for; the National Association

of Energy Service Companies (NASECO), http://www.naesco.org/index.htm and the Energy Service Coalition (ESC) http://www.escperform.org/.

NAESCO, the major ESCO trade association, has a Web site offering

information to better understand the process, the pitfalls and answers

to many other questions. NAESCO, ESC and the Association of Energy Engineers offer Web resources and sponsor seminars throughout the year.

The ESC is a national nonprofit organization composed of experts from

wide ranging organizations working, at state and local levels, to

increase the number building energy upgrades completed through

performance contracting. This organization also offers sample

documents like Request for Proposals or performance contract

documents. The ESC Web site also has list of providers and other

industry professionals. The LBNL study also has good basic

information and it may be downloaded at http://eetd.lbl.gov/ea/EMS/EMS_pubs.html.

The Next Wave

The adoption of IT related nomenclature to describe Next Generation Buildings

represents awareness that buildings are huge consumers of energy,

particularly electricity. Among many important data points is

buildings make up as much as half of electricity consumption in the

US. Energy Information Administration (EIA) puts buildings at 17%

of US energy consumption overall, but buildings alone account for 35%

of electric consumption, thus the building industry is very important

to electricity companies. On the flipside, EIA data also

indicates that electricity represents 75% of the energy bill for

commercial buildings, and presents some real impact on occupants in a

number of ways. Power outages decimate productivity, according to

EPRI they cost US businesses $80 billion per year and detract from

comfort and environmental safety by interrupting HVAC.

Targeting the

energy cost metric, the first ESCO wave completely focused on

efficiency and third party financing, but this next iteration will

address new funding opportunities from the other side of the meter.

McGowan coined the term “Electricity Capital” to address this new

category of funding opportunities. Electricity Capital is relatively

new as Electric utilities across the country are creating all sorts of

mechanisms to promote implementation of buildings energy

projects. There are a host of drivers including: Renewable

Portfolio Standards, Commission Mandates, forecasts that predict

electricity demand to grow as economic recovery unfolds, etc.

One example is

that a number of utilities, both electric and gas, offer on-bill

financing for efficiency projects including BAS. Quite simply the

building owner may be able to finance a building automation or other

efficiency measure on the utility bill. Similarly Property

Assessed Clean Energy (PACE) has been reborn offering funding to

building owners for such improvements by increasing their property

tax. These programs, along with a resurgence of interest in

energy, coupled with scarce capital from traditional sources have led

to more alternative financing models like Energy Services.

Many ESCO’s are

teaming with Smart Grid and utility rebate experts to provide turn-key

solutions. Of course many building automation manufacturers are

already ESCO’s, but more contractors are also adopting this model all

the time. At the heart of all these new trends are smart building

technology and “cloud” based software applications to enable the

building to save more and fund projects, as well as perform analytics

that are necessary to validate the performance.

Electricity

Capital comprises programs like Demand Response (DR) that pays

customers to respond to curtailment events through deployment of

strategies in the BAS to shed load. OpenADR™ is the standard developed

at Lawrence Berkley Labs, which many are aware of, but exhibitors at

far ranging events including: AHR Expo, Niagara Summit, Realcomm/IBcon

and the World Energy Engineering Congress are touting their ability to

integrate OpenADR into BAS just like BACnet™ or LON™. Some

manufacturers provide pre-programmed Demand Response Algorithms,

working with customers to deploy DR creating a revenue stream to fund a

BAS. One DR provider has completed projects with multi-location

customers that are paying for DR enablement and a new BAS with

Electricity Capital. Under this model the owner gets technology

installed with no upfront cost and is able to finance the deployment

and repay it through DR payments from the utility over time. Stay

tuned because Electricity Capital will grow to include a wide range of

additional funding mechanisms for the savvy owner and provider.

With ESCO 1.0 no

one disputes that efficiency investments made by building owners are

“bankable” and cost effective. These investments also help

utilities, but only with one of their two concerns. When

considering electricity, there are two important topics; energy use and

energy demand. Efficiency helps utilities with energy use and it

makes sense to optimize building energy consumption because it reduces

operating cost. Electric demand growth and emerging electricity

markets present new utility concerns, and most building owners are

unaware of the financial benefits they can offer. Those managers

with graying temples remember demand limiting, etc. from the 1980’s,

but that is just part of the story. It is a shock that 25% of the

multibillion dollar electric infrastructure (power plants, transmission

and distribution lines, etc.) exists to keep the lights on for just

~100 hours/year of peak demand. That’s because the monopolistic

electricity business model traditionally sets one price for units of

power, $ / KWh, no matter when it is consumed. The Demand Charge,

$ / KW, is applied to commercial bills, but that does not begin to

match wholesale electric price volatility before, during and after

periods of peak electric use.

ESCO 2.0 is about

tapping into fees that utilities are willing to pay the owner for

developing strategies to support the utility in keeping the lights

on. ESCO projects have typically generated two types of savings;

“energy” and “operations and maintenance, the 2.0 with generate a new

type cash flow that is not “savings” but “income”. Demand

Response is an early example of this income that has been widely

embraced, but that is just the beginning. Utilizing the same

technology that has been put in place to enable demand response, many

electricity users have begun to offer capacity back to the grid at peak

times… for a price. The price is income. In summary, these

Income strategies combined Savings strategies can create the

opportunity for larger and more exciting ESCO projects.

[an error occurred while processing this directive]A

key point that can be overlooked here however is that the 2.0 in ESCO

2.0 is first an indicator that this is truly a next generation business

model. Central to this model however is also the deployment of

next generation technologies. ESCO 2.0 will provide a mechanism

to achieve Smart Buildings, and with the Energy Techno-Strategies

deploy by local, and cloud based technology, the building with be an

energy profit center by participating in both efficiency and the

electricity markets. Quite simply as shown here ESCO 2.0 will be

made up of Smart buildings that use energy in Clean, efficient and cost effective ways and are therefore Green

buildings, but more importantly they are green in the environmental

sense, as well as in the economic sense. Those buildings that

integrate more functionality in will benefit from more robust the

participation. ESCO 1.0 Buildings often overlooked the Smart

Clean Tech implementation, but 2.0 will start with commissioned,

effectively operated BAS, electric sub-metering, dashboard technology

to visualize building performance and analytics to evaluate performance

over time and develop benchmarks for comparison. Buildings

enabled like this can participate in demand response (DR) immediately

by implementing technology to receive electronic “event notifications”,

via the OpenADR standard, when demand response events are called.

The building then reacts to that event by modifying equipment operation

to reduce an agreed upon number of KW. Programs vary in the

amount of notice that customers receive, usually “day ahead”, “day of”

or “10 minute” notice. Programs also vary in the amount of money

paid for participation but customers typically receive payments between

$50 and $300 per KW. For example, a 200 KW enrollment would net

an annual payment between $10,000 and $60,000. With most programs

a customer gets paid whether an event is called or not, and in

California the utilities will even pay to install the technology.

That all sounds pretty good, but it is just the beginning. This

same Smart Grid/DR technology can be used to enable customers to sell

electricity, they agree not to use, back to electric markets. We

call this “day trading for energy”, and it gives customers another way

to leverage financial value from Smart Grid. Adding this income to the

Arbitrage mix will create those larger projects.

At first building

owners may think this is too complicated and maybe it’s not worth

it. The same could have been said of many technologies now widely

used, when they were first introduced. That could also be said of

green building recognition systems that have become the norm.

Even more compelling, customers that leverage these technologies and

programs effectively, can literally spin the meter backwards,

while at the same time leveraging third-party capital and make debt

service with REC payments from the utility and cost reduction on energy

bills while optimizing building performance and tenant comfort.

The ideal scenario is when customers go further and expand building

technologies to include; energy storage: thermal or battery, onsite

generation, or what are now called “microgrids”. The idea is to

take the renewed challenges many parts of the country are facing with

electricity reliability, and apply entrepreneurship to turn buildings

into profit centers for energy. Demand Response (DR) has

gotten a great deal of traction and is paying dividends for many

building owners, but the next step is to insulate the tenants from any

inconvenience that might be caused by DR. This is done by

leveraging automation systems to pre-cool for example, focusing

strategies on shutting down nonessential equipment, and leveraging

onsite generation, but numerous other options exist. Using

advanced DR and OpenADR based technology, owners can also aggregate

across multiple buildings and Opt In or Opt Out based on what is going

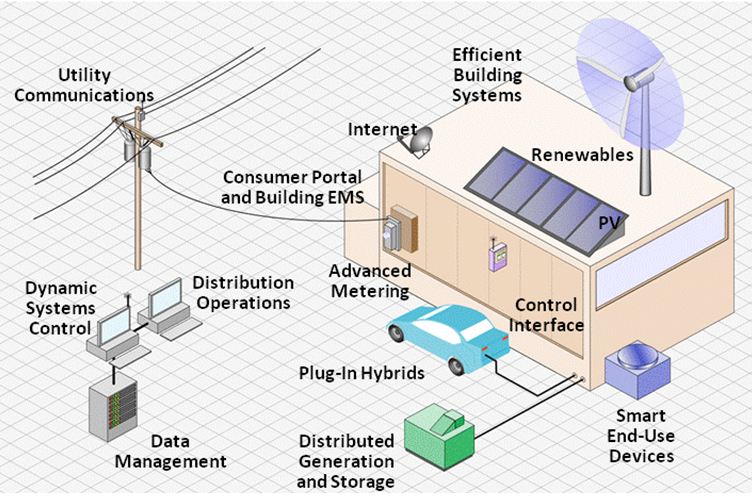

on in the building. Owners. The picture here comes from the

Electric Power Research Institutes “Green Grid” report and begins to

show the myriad technologies that are being applied to any size

building. The challenge in today’s economy is finding ways to

fund these technologies and ESCO 2.0 could be the answer. Equally

exciting is that owners can leverage the intelligence deployed in these

systems to make performance repeatable, and to apply analytics that

make it possible to evaluate the project in real time, not just once a

year. All of these ideas mean that ESCO 2.0 amounts to free money

and no one can afford to turn that down in this economy.

About the Authors

John

J. “Jack” Mc Gowan, CEM

John

J. “Jack” Mc Gowan, CEM

Jack McGowan is President of Energy Control Inc. (ECI), an OpTerra

Energy Group company and is Chairman Emeritus of the U.S. Department of

Energy GridWise Architecture Council and Ambassador for the OpenADR

Alliance for Demand Response. He is on the Galvin Electricity

Initiative Team of Leaders and was Founding Co-Chair of the National

Institute of Standards and Technology Building to Grid Working

Group. McGowan is working with ESCO 2.0, Demand Response and

Smart Grid Projects across the US. The Association of Energy Engineers

admitted him to the “International Energy Managers Hall of Fame” in

2003 and named him “International Energy Professional of the Year” in

1997. ECI won a 2008 American Business Award sponsored by Dow

Jones and the Wall Street Journal as Best Overall Company in the U.S.

with less than 100 employees. Mc Gowan is an author with 5 books on

Fairmont Press and Prentice Hall and over 200 articles. He also

sits on the Technical Advisory Board of Engineered Systems and is a Contributing Editor with www.automatedbuildings.com.

Leighton J. Wolffe

Leighton J. Wolffe

Leighton Wolffe is

the Principal of Wolffe Technology Group LLC, an independent consulting

organization providing strategic business development, market research,

and technology assessment services. WTG serves the facility industry as

an owners advocate for Federal and State Agencies, health care

institutions, universities, corporate real estate, and high tech

environments.

WTG works with

facility owners to develop and manage portfolio wide energy and capital

upgrade projects utilizing new technologies, products and services

through traditional and innovative financing models and energy market

programs.

As a research and

development firm, WTG provides investors and companies with

perspectives on emerging market trends, technology applications,

business models and product design. WTG works with clients to establish

and deploy successful strategic marketing and business development

initiatives for their products and services into existing and new

markets.

Wolffe began his

career in facility operations in hospitals and universities, later

working with manufacturers of building automation systems, and more

recently with energy companies and hi-tech startups to develop new and

innovative products and software applications. He has authored numerous

articles on evolving energy trends, serves on technology advisory

boards, is a featured speaker at industry events and is active in all

US competitive energy markets.

References

[1] http://en.wikipedia.org/wiki/User-centered_design User-centered design

footer

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The

Automator] [About] [Subscribe

] [Contact

Us]