|

September 2019 |

[an error occurred while processing this directive] |

| Accommodating

Private Capital Markets It's a Great Time for Business Owners to Raise Capital or Consider an Exit |

Glenn Tofil, Managing Director England & Company |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

Despite wild daily swings in public equity markets,

emerging global

economic headwinds, and geopolitical uncertainty, merger and

acquisition and financing activity involving privately-held companies

in the US remains strong, especially

within the intelligent building sector.

Abundant

equity and debt capital are available to private business owners to

fund growth initiatives, and private equity investors (fueled by nearly

$570 billion of unused and available capital

commitments and strategic acquirers with under-levered balance sheets are providing a

highly liquid market for business owners considering an exit.

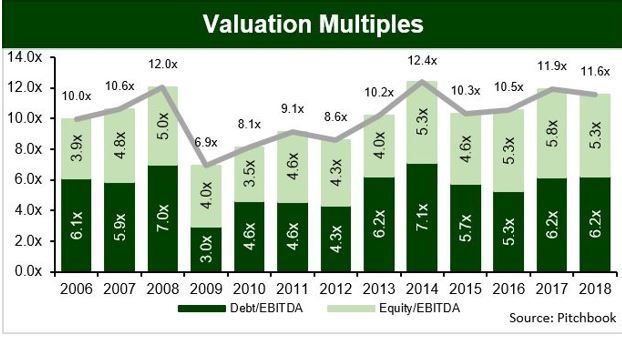

According to Pitchbook,

this abundance of capital, coupled with accommodating low interest rates and the

willingness of debt capital providers to support transactions, has

driven average middle-market transaction valuation multiples

of

Earnings Before Interest, Taxes, Depreciation, and Amortization

(“EBITDA”) from approximately 7.0x EBITDA in 2009 to nearly 12.0x

EBITDA in 2018.

Private capital markets continued their strength during the first half of 2019. However, we believe that business owners considering a financing transaction, or an exit, should be mindful of where we are in the macroeconomic cycle and that buoyant and accommodating private capital markets may not continue indefinitely. For business owners in the intelligent building sector, we cite the following when considering the timing for accessing the private equity and debt markets for growth or considering an exit.

The Positives:

The Negatives:

Our Conclusions:

While

England & Company is not calling a top in the market or any

type of dislocation like we saw in 2008, we do believe that we are very

long in a highly accommodative cycle in the private capital markets and

it is definitely our feeling that market conditions will not

appreciably improve from their current level. Therefore, if you

are considering a capital raise to fund an acquisition or organic

growth initiative or even an exit, we feel that there is no time like

the present to explore your options.

About the Author:

Glenn Tofil is a Managing

Director with England & Company. He focuses on power,

industrial, and infrastructure technology and services markets.

Glenn has significant experience working with shareholders and

executive teams of middle-market companies to create long-term value

through mergers and acquisitions and private capital raising

transactions. He can be reached by email at

gtofil@englandco.com.

About England & Company:

With

offices in Houston, New York, and Washington, DC, England &

Company is an independent investment banking and advisory firm

dedicated to the middle market. Since the founding of England in 2003,

the firm has provided honest and effective advice on mergers and

acquisitions, private capital raising, financial restructuring,

fairness oinions and valuations, and strategic advisory to the

executive teams, boards of directors, and financial sponsors of public

and private companies.

Please

visit England & Company’s website for more information on our firm and to

download the latest edition of our Growth Wire Report on the

Intelligent Buildings Sector.

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]